Who says A must say B

Perry Mehrling, Nathan Tankus and a handful of friendly collaborators are to be credited with most of the ideas presented here. All errors are mine. I thank my friend and future co-teacher Jens for inspiration.

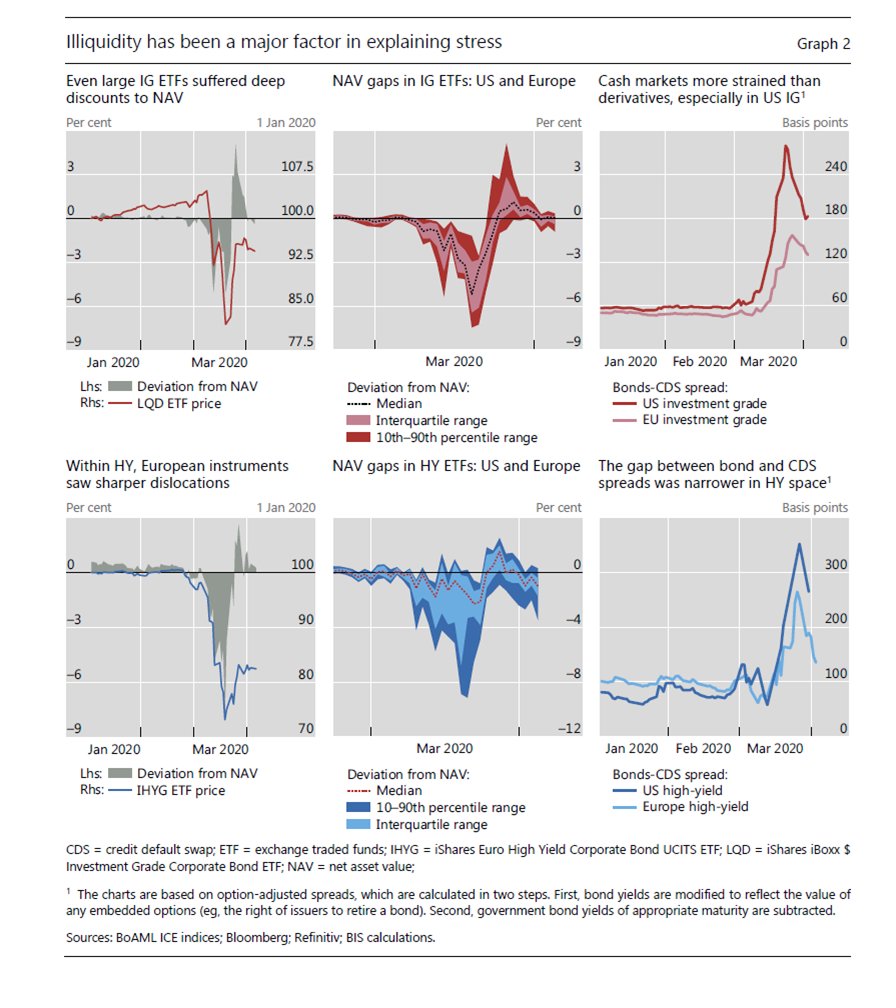

A recently published (April 14) BIS note with the name BIS Bulletin, No. 6: The recent distress in corporate bond markets: cues from ETFs by Sirio Aramonte and Fernando Avalos has captured much of my attention this week. The note contains amazing graphs showing the recent stresses in corporate debt markets, provides a justification for the Federal Reserves’ (“Fed”) support of the high yield (“HY”) market in the US, and, so I believe, provides evidence that the technocratic institutions governing global high finance are working well. And that is good news!

Let’s look at the pictures first. The graphs on page 2 make the stresses that the corporate bond markets went through in recent weeks visible at one glance. For both investment grade (“IG”) and HY debt the spreads blew out first at the end of February and then again in mid-March. More so in the US than in Europe and much more so in HY than in IG (check the basis points scales).

The graphs on page 3 focus on the deviation of prices from net asset values. The dislocations in European HY were particularly sharp (bottom left corner). And again, the stress begins at the end of February and escalates in mid-March.

The BIS note describes the impact of the C-19 crisis on European and US exchange traded funds investing in corporate bonds, and from this description derives insights on the functioning of the corporate bond markets at times of heightened stress. There are two main messages: The bond markets were illiquid in mid-March, i.e. nobody wanted to trade/buy bonds because the impact of C-19 brought so much uncertainty upon the market. Things were pretty bad. Then, things got worse. In the US, a lot of money flew out of the bond markets when the Fed announced its Money Market Mutual Fund Liquidity Facility (“MMMFLF”) on March 18. So the authors make the point that a deliberate policy action by the Fed in one part of the market caused a distortion in another part of the market. That’s a pretty big deal!

This is to be understood in the context of the Fed’s April 9 announcement in which the Fed said it will now also support the US HY market by buying shares in exchange traded funds that own HY bonds and seek to track the market (NB: the purpose of these asset purchases is to support the HY market, yet the Fed is not directly taking HY bonds onto its balance sheet). After this announcement there has been a very vibrant (Twitter) debate around whether the Fed should support the HY market. Some are of the opinion that the privilege of central bank support should be exclusively extended to “better” debt. There is a lot to this argument given that it is easy to take this stuff onto the balance sheet and difficult to get rid of it later. Others have said, it is necessary to support HY debt because there is so much of it and you do not want all of these companies and investors go belly up. Also, the distinction between HY and IG can be a blurry line, especially during these times. There is a lot to all these arguments. The BIS note takes side with the Fed and implies that the Fed had to support the HY market because the Fed’s own actions created some of the distortions in this market. The argument being, who says A must say B.

Can we expect other central banks, such as the ECB and/or the BoE to also support HY markets with similar actions? The European HY market, which so far has only shown one tiny little sign of life last week, would roar. My guess is—and I may be mistaken—that will not be the case. I am thinking that given that bank lending in Europe is so much stronger than in the US, the ECB and the BoE will not feel compelled to support the HY market. Another argument that there is no need for them to step up, is that public investment banks, such as the EIB, Instituto Credito Oficial, British Business Bank, and KfW, are much stronger in Europe than in the US. Finally, in the case of the ECB, it made its announcements quite early in the crisis and gave the impression that there will not be any new announcements any time soon, including no announcements re the HY market.

Generally, if market supporting actions by central banks create distortions, which other distortions do we have to expect? Again, I may be mistaken but something that comes immediately to mind is the global south. I would guess that the money flight from the global south and the emerging markets will be worse this time than in 2008. We are already seeing this to some degree but I believe it may get worse. In 2008 there was less (and later) central bank support for markets in the global north. So there was less imminent reason to pull money from the south and take it into the “central bank supported safe havens” in the north. In an analogy to how money left corporate bond markets and went into MMMFs in March 2020, one could argue that given that we are seeing unprecedented central bank support in the global north, there is now more incentive to flee from the south than in 2008 and to do so rather sooner than later.

From a political economy perspective, the BIS note being published only five days after the Fed’s announcement evidences that the technocratic governance machine of global money is working. And it is working well! One would be mistaken to believe that someone in Basel was doing research, looking at corporate debt markets blow out in March, and then called up the Fed to urge them to take action and save the HY market. One would equally be mistaken to believe that the Fed saw corporate debt markets blow out after it launched the MMMFLF, came up with a plan to support the high yield market, and then called up the BIS and urged them to publish a research piece justifying the Fed’s actions relying on the BIS’ credibility as the central bankers’ bank (rather than on the research arm of the NY Fed or the US Treasury’s Office of Financial Research). The timing of the note publication suggests that the Fed and the BIS are talking, that they are in deep conversation about how the global financial system should be run so it can weather the crisis. And that is a good thing! Given how powerful central banks are in today’s world, and how removed and isolated they are from democratic control, we can only hope that the informal conversations that these technocrats are having among themselves put checks and balances on them, make them accountable to each other, and allow them to take the most consequential of all actions only after much deliberation, if not, after a consensus has emerged.

Historically, the type and quality of conversations the Fed and the BIS and a handful of other central banks are having seem to be what distinguishes 2020 from 1931, when the world entered a global depression. Then, the BoE, at the time the most powerful central bank in the world, was not part of such a global debate. When Germany ceased reparation payments and the global financial crisis escalated, the BoE decided to prioritize the management of the domestic financial crisis. It did not throw swap lines to other major central banks nor did it manage international money flows but it rather went off the gold standard. The embeddedness of the Fed into a global conversation on international finance, a seemingly tiny, maybe even ivory tower-like detail is one of the factors ensuring that we are headed for a global recession and not for a global depression.

Maria C. Schweinberger